Following the Trump administration's "Liberation Day" announcements on April 2, worries about new tariffs on pharmaceutical products—historically exempt from such duties—have pushed drug companies to make unprecedented commitments to U.S.-based production.

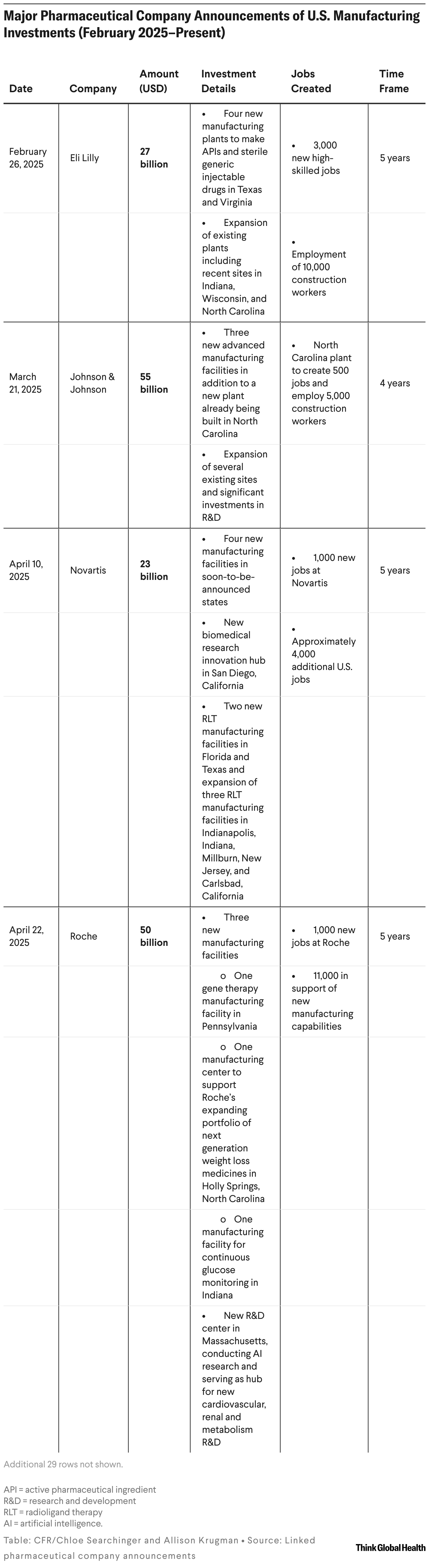

Even before pharmaceuticals became a tariff target, firms were bracing for a reshoring agenda. In late February, Eli Lilly announced a $27 billion effort to expand domestic manufacturing of active pharmaceutical ingredients (APIs) and sterile injectables. Since then, 13 additional companies have announced investments—pledging a total of more than $480 billion over the next 4 to 10 years.

Their promises came amid a prolonged pressure campaign. The administration launched Section 232 investigations on pharmaceutical products and medical devices, which could result in trade restrictions on those imports. In September, the White House threatened 100% tariffs on companies not planning to build U.S. facilities, despite reaching a deal the same month with Europe to cap drug tariffs at 15%.

The investment announcements include the establishment of 22 new manufacturing sites, citing the generation of approximately 44,000 new jobs. These efforts plan to span various products and drug categories—APIs and sterile generics, radioligand therapies, gene and weight-management therapies, biologics, small molecules—offered from major companies including AbbVie, AstraZeneca, Bristol Myers Squibb, Eli Lilly, Gilead, GSK, Johnson & Johnson, Merck, Novartis, Novo Nordisk, Pfizer, Roche, and Sanofi.

However, if pharmaceutical companies are steadfast about their new capital investments, their announcements should create a trickle-up effect whereby tangible expansion occurs in the procurement of upstream equipment. To build new biopharma plants and produce biopharmaceuticals, the companies need obtain consumables, reactors, bioprocessors, pipes, mixers, and other specialized infrastructure essential to drug manufacturing. It is also unclear how many of these putative sites—and what share of the pledged funding—are truly greenfield (built from scratch) versus brownfield (repurposed) or acquired from other owners is not evident from the announcements.

We assess the materiality and saliency of these declared investments—in the short to medium term—by tracking whether the announcements have translated into capital spending and demand for drug manufacturing equipment.

The publicly traded companies behind this equipment should likely indicate anticipated revenue and demand growth to their shareholders and investors. Even a conservative estimate that 15% of this capital expenditure will go toward purchasing such bioprocessing equipment would amount to more than $75 billion—an unprecedented upswing in revenue for manufacturers of this equipment.

If the bioprocessing equipment market does not fully internalize this surge in demand, it could spawn shortages on par with those experienced during COVID-19—when drugmakers pushed to expand capacity for vaccine and therapeutic development. This period witnessed widespread scarcity for single-use reactors, filters, and other key components of drug manufacturing. Tightening the global market for bioprocessing equipment and consumables could create significant challenges for manufacturers that supply vaccines to international agencies such as Gavi and the Vaccine Alliance and for those involved in pandemic-readiness products when reliability and uninterrupted availability are critical to protecting lives and the economy. When shortages occur, the poorest country markets are underserved.

Manufacturers of Upstream Construction Equipment

Pharmaceutical

company

announcements

Upstream

equipment

suppliers

Equipment type

AbbVie

Amgen

AstraZeneca

Bristol Myers Squibb

Eli Lilly

Gilead Sciences

GSK

Johnson & Johnson

Merck

Novartis

Novo Nordisk

Pfizer

Roche

Sanofi

Corning

Cytiva

Eppendorf

Merck KGaA

Millipore

Pall Corp.

Purolite

Repligen

Sartorius

Thermo Fisher Scientific

Univercells

Bioreactors and fermenters (stainless steel and single-use systems

Mixers and preparation systems

Filter and perfusion systems (Alternating Tangential Flow, ATF; Tangential Flow Filtration, TFF)

Single-use containers and assemblies (bags, tubing, connectors)

Cell culture media and feeds

For the purposes of the analysis throughout this piece, Danaher Corporation is the parent company of Cytiva and Pall; Millipore is a subsidiary

of Merck KGaA; Purolite is owned by Ecolab. Univercells and Eppendorf are not publicly traded, and are therefore excluded from analysis.

Chart: CFR/Chloe Searchinger and Allison Krugman • Source: BioProcess International

AbbVie

Amgen

AstraZeneca

Bristol Myers Squibb

Eli Lilly

Gilead Sciences

GSK

Johnson & Johnson

Merck

Novartis

Novo Nordisk

Pfizer

Roche

Sanofi

Pharmaceutical

company

announcements

Corning

Cytiva

Eppendorf

Merck KGaA

Millipore

Pall Corp.

Purolite

Repligen

Sartorius

Thermo Fisher Scientific

Univercells

Upstream

equipment

suppliers

Bioreactors and fermenters (stainless steel and single-use systems

Mixers and preparation systems

Filter and perfusion systems (Alternating Tangential Flow, ATF; Tangential Flow Filtration, TFF)

Single-use containers and assemblies (bags, tubing, connectors)

Cell culture media and feeds

Equipment type

For the purposes of the analysis throughout this piece, Danaher Corporation is the parent company of Cytiva and Pall; Millipore is a subsidiary of Merck KGaA; Purolite is owned by Ecolab. Univercells and Eppendorf are not publicly traded, and are therefore excluded from analysis.

Chart: CFR/Chloe Searchinger

and Allison Krugman • Source:

BioProcess International

Statements on Future Growth and Earnings

Our analysis compiled and examined the earnings reports from seven upstream suppliers of pharmaceutical equipment, made during the first quarter (Q1), Q2, and Q3 of 2025. Each equipment supplier has a unique size and revenue makeup, but their earnings statements should reflect expectations for future high growth.

Little mention about upticks in procurements from onshoring was made during earnings calls held in Q1 and Q2. However, the most recent quarter—Q3—did see some discussion of growth opportunities from onshoring announcements, suggesting that bioprocessing equipment companies are cautiously optimistic about future demand from the manufacturing capacity announcements.

The time lines for new orders, though, remain uncertain amid fluctuating policy from the administration. When asked about U.S. pharmaceutical investments during a November conference, Repligen CEO Olivier Loeillot was more direct, saying that even a fraction of the total announcements, or $50 to $100 billion, would still offer high-growth potential for the equipment industry, and that time horizons for breaking ground were 2026 and 2027 at the earliest.

Share Prices as Indicators of Rational Expectations?

The stock market can often reflect rational expectations for future earnings growth, so in theory it should anticipate the increase in revenue among equipment manufacturers that billions of dollars in investment in new manufacturing plants would yield. If a policy change or major event is likely to increase a company's revenues substantially in the future, its stock prices should react.

This pattern should occur even if real revenue has not yet increased—and even as companies and the contract and development and manufacturing organizations (CDMOs) that facilitate contracts for purchasing await tariff policy enacted at executive level to become firmer.

To assess these trends, we analyze the share prices of all the publicly listed bioprocessing equipment companies, starting from the early days of the Trump administration through mid-November. This time frame should capture the influence of the Liberation Day tariff announcements on April 2.

Except for Eli Lilly and Johnson & Johnson's investment announcements in February and March, most of the pledges occurred after Liberation Day. The rest of April and May saw pledges accrue to $155 billion, and another $180 billion has been announced since mid-September.

Relative share prices, however, have decreased on average or returned to similar pre-Liberation Day levels. Corning Incorporated is the only outlier, seeing its stock rise to 180% of its original value since early April from massive growth in its AI fiber optics technology. Admittedly, other factors could be affecting these companies' stock prices, including postpandemic recovery as excess equipment sales during the pandemic are resold. Some are diversified firms for which bioequipment is only a small percentage of total revenue. Another reason the stock prices have not responded to the announcements is that investors could still be shrugging off the tariffs, expecting erratic threats from the administration to simmer and negotiations to reduce market impacts.

Nevertheless, a single event that could add up to $75 billion to an industry consisting of a few major players should affect share prices.

Investments Do Not Equal Resilience

Time will tell how companies react to this policy uncertainty. Current corporate statements and the lack of significant stock market movement suggest that equipment suppliers are uncertain whether and how many facilities will break ground in the near future despite the capacity expansion announcements. The bioprocessing and bioequipment manufacturing sector still appear to be cautious about the scale of growth.

What products and plants will benefit most from these investments remains unclear, raising questions about where Section 232 tariffs or concerns of national security could come into play.

If these expansion projects never materialize, they could muddy genuine efforts to plan capacity in areas where the United States needs greater resilience, such as strengthening its supply chain for staple antibiotics facing routine shortages. The United States could also fall behind competitors. Along with its output for antibiotics and small molecule products, China has also been rapidly expanding its capabilities in antibody drug conjugates for cancer and oncology—by investing heavily in manufacturing capacity and regulatory pathways that support fast development.

To ensure resilience in the market, all future capacity expansion should not flow only into the most advanced areas, such as cell and gene therapy. These fields are undeniably important, but a concerted focus is also needed to prevent the antibody-drug conjugate and monoclonal antibody markets—two rapidly evolving classes of therapeutics—from falling into the same fragile position as today's small-molecule fermentation sector, which depends heavily on China and India for generic drugs and antibiotics.

The purpose of the 232 tariff invesitgiations is to strengthen resilience, which means directing new capacity to the U.S. areas that need it most, not simply supporting expansions that could have happened anyway in response to market growth—the only change being the shift in location from the EU to the United States.

Another question is where the necessary talent and long-term workforce will come from to support $480 billion investments in U.S. manufacturing capacity for advanced therapeutics. The pledges aim to create nearly 44,000 jobs. Are universities and training institutions internalizing this future growth alongside bioprocessing companies?

Advanced biomanufacturing requires experienced professionals who have spent years working in major companies or manufacturing hubs, and many of these breeding grounds are not located in the regions where new facilities are being announced. This discrepancy could call significant workforce movement including relocations from the European Union to the United States, as well as labor migration within the United States. True resilience in the pharmaceutical sector requires more than announcements of new facilities. It demands strategic investments and targeted capacity building, coupled with a long-term plan to develop the workforce and ecosystem needed to sustain U.S. leadership in biomanufacturing.